The reported financial statements for banks are somewhat different from most companies that investors analyze. For example, there are no accounts receivables or inventory to gauge whether sales are rising or falling. On top of that, there are several unique characteristics of bank financial statements that include how the balance sheet and income statement are laid out. However, once investors have a solid understanding of how banks earn revenue and how to analyze what’s driving that revenue, bank financial statements are relatively easy to grasp. In these first two examples, assets and liabilities both change by equal amounts.

The following balance sheet is a very brief example prepared in accordance with IFRS. It does not show all possible kinds of assets, liabilities and equity, but it shows the most usual ones. Because it shows goodwill, it could be a consolidated balance sheet. Monetary values are not shown, summary (subtotal) rows are missing as well. Historically, balance sheet substantiation has been a wholly manual process, driven by spreadsheets, email and manual monitoring and reporting.

Stock selection

Substantially higher loan and lease losses might cause a bank to report a loss in income. Also, regulators could place a bank on a watch list and possibly require that it take further corrective action, such as issuing additional capital. Also, as interest rates rise, banks tend to earn more interest income on variable-rate loans since they can increase the rate they charge borrowers as in the case of credit cards.

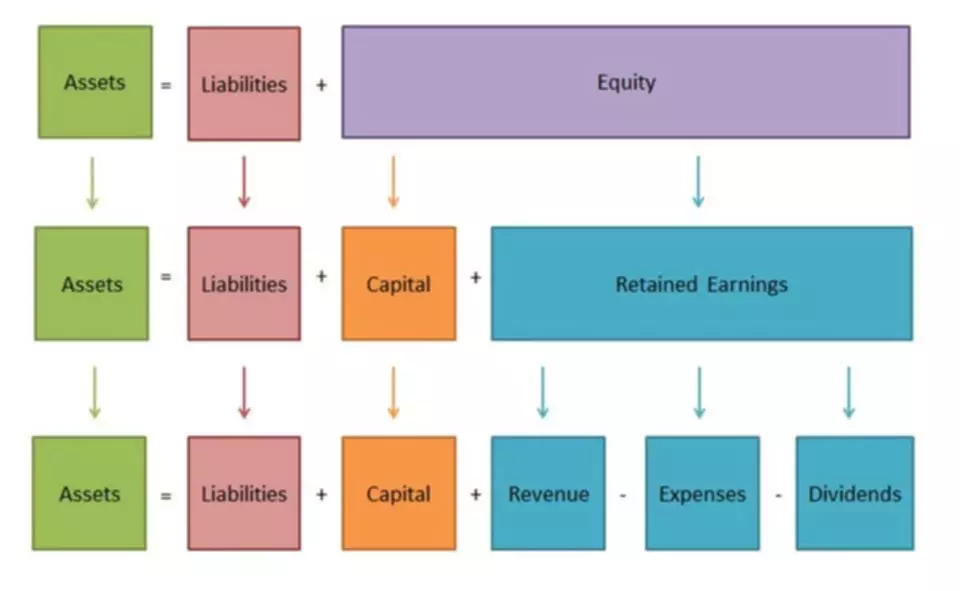

- A liability is any money that a company owes to outside parties, from bills it has to pay to suppliers to interest on bonds issued to creditors to rent, utilities and salaries.

- Bank’s Balance sheet comprises of three parts assets, liability, and equity.

- And then in the final part you got practice yourself with calculating regulatory capital.

- On the other hand, if the bank’s leadership seems like a scandal-magnet, and the culture rewards higher risk, you might want to subtract 2% or more of the fair value of all level 3 assets.

- You’ll see the dollar amounts on the right — as the interface notes, all dollar amounts are displayed in thousands, so add three zeros to all the dollar amounts you see.

The first step in preparing financial statements is to sum the activity that has taken place in each of the accounts during the period. Following the trial balance, a number of closing entries are made to the accounts. A balance sheet is a financial report that shows how a business is funded and structured. It can be used by investors to understand a company’s financial health when they are deciding whether or not to invest.

Bank Capital

This tells us that 75.87% of DaimlerChrysler’s assets are debt financed. Notice that this ratio is slightly less than the 77.7% we calculated on the unadjusted balance sheet. The argument for not doing this is that in a PFI-Model contract other economic-ownership risks are taken by the Project Company, and it is thus similar to an operating lease; but as the discussion below will show, this is a very grey area. It is probably questionable whether a black-and-white decision—on or off the public-sector balance sheet—is appropriate, since it is clear that a PPP involves complex gradations of risk transfer. There is an argument for a more sophisticated approach which reflects this and would divide the balance-sheet recording between public and private sector. Thus, capital regulation is justified as an attempt to correct the market failure that results from banks’ preference for a higher debt/equity ratio than is socially optimal.

The classic is Mario Draghi’s “whatever it takes”, where the ECB provided a backstop for euro area sovereigns but ended up buying nothing. Another is the Bank of England’s 2009 operations in sterling corporate bonds; these were not zero, but small. The Federal Reserve’s Secondary Market Corporate Credit Facilities is a third example. Originally announced on 23 March 2020 and expanded two weeks later, risk spreads and bid-ask spreads shrunk immediately (Gilchrist et al. 2020). While authorisation was for $750 billion, the Fed’s holdings of corporate bonds and exchange-traded funds (ETFs) peaked at $14 billion6 – and could, perhaps, have been smaller. A bank that is bankrupt will have a negative net worth, meaning its assets will be worth less than its liabilities.

Transaction H

However, it should not be excessive, since capital in the form of long-term assets usually has a higher return. The excess of the bank’s long-term assets over its long-term liabilities is an indication of its solvency, its https://www.bookstime.com/articles/financial-statements-for-banks ability to continue as a going concern. That’s because a company has to pay for all the things it owns (assets) by either borrowing money (taking on liabilities) or taking it from investors (issuing shareholder equity).

The net worth is the asset value minus how much is owed (the liability). A bank has assets such as cash held in its vaults and monies that the bank holds at the Federal Reserve bank (called “reserves”), loans that are made to customers, and bonds. They also show how much of the bank’s deposits are actually covered https://www.bookstime.com/ by federal deposit insurance versus uninsured deposits. A few examples reveal the usefulness of this key accounting relationship. Starting with individuals, the following table reports the balance sheet for all U.S. households at the end of 2021, with assets on the left and liabilities plus net worth on the right.

User account menu

So we are just going to take our Net Income and then divide by the average Total Assets right here. Now let’s go over here and look at some of these other metrics and ratios. For some of these, you are going to be using averages, so you have to be a bit careful. For the Net Charge-Off Ratio, let’s take the number here and then divide by the average Gross Loan balance. And then our Gross Loans are also going up by a fair amount, our Cash balance going down, but that doesn’t really matter because the cash itself is not going to factor into regulatory capital in that way.

A balance sheet explains the financial position of a company at a specific point in time. As opposed to an income statement which reports financial information over a period of time, a balance sheet is used to determine the health of a company on a specific day. In this example, Apple’s total assets of $323.8 billion is segregated towards the top of the report. This asset section is broken into current assets and non-current assets, and each of these categories is broken into more specific accounts. A brief review of Apple’s assets shows that their cash on hand decreased, yet their non-current assets increased. This financial statement lists everything a company owns and all of its debt.